When "Promising" Becomes Dangerous

The most dangerous startups are not always the ones where nothing is working.

Those are painful, but at least they are clear.

The harder ones are the startups where something is kind of working.

A customer is interested, but not urgent. A pilot is active, but not expanding. Revenue exists, but every dollar requires custom work. Users like the product, but only when the founder is personally involved. Investors are excited, but keep saying, “Let’s stay close.”

None of these are hard no’s.

That is what makes them dangerous.

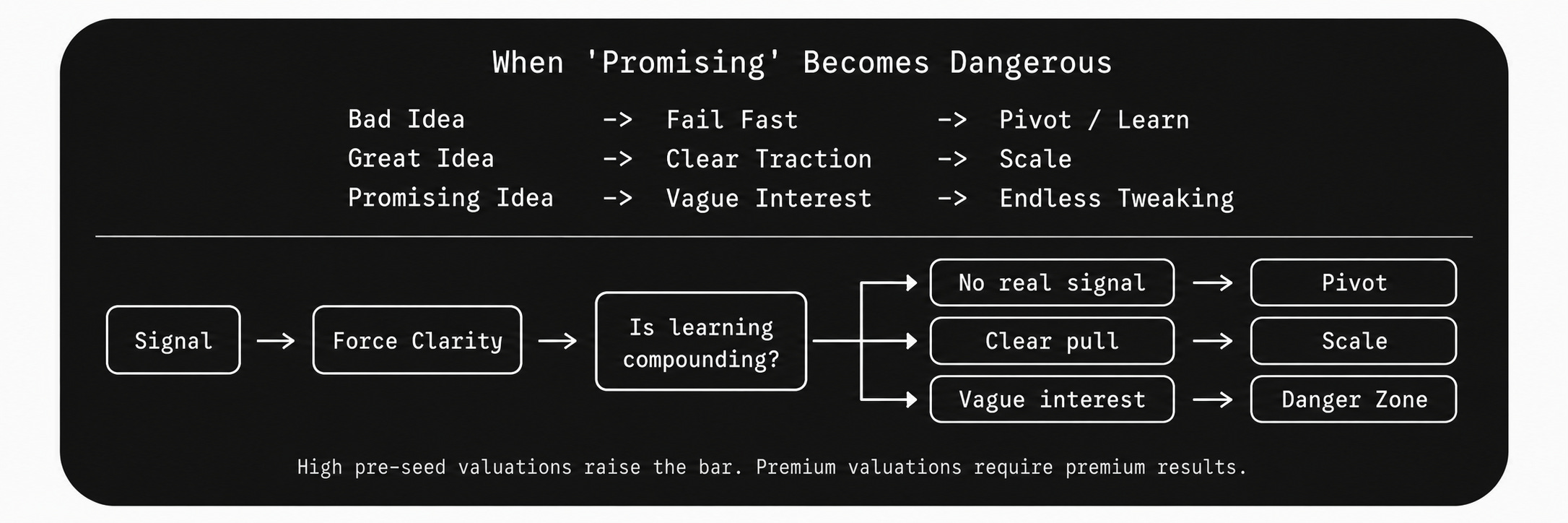

Promising is not the same as working.

Promising means there may be something there. Working means the signal is getting stronger, clearer, and easier to repeat.

The danger is that promising can keep a founder busy long after the company should have forced clarity.

The trap is partial success

If nothing is working, the answer becomes obvious: you have to change.

But if something is somewhat working, the decision gets harder.

A founder signs a $10K paid pilot with a mid-market customer. It is not life-changing revenue, but it is real. The team celebrates because for the first time, the market feels like it is saying yes.

Three months later, the pilot is still “going well.” The champion likes the product. The weekly calls are positive. But no one owns the budget, the VP has not engaged, and every conversation ends with one more feature request.

The founder keeps building because the customer feels strategic.

Six months in, the company has revenue, but not repeatability. The product is better for one customer and harder to sell to the next ten.

That is when promising becomes dangerous.

Not because the founder is lazy. Usually the opposite. The founder is working constantly.

The problem is that all of that work is going into extending the current version instead of asking whether the current version deserves to continue.

The better question is not: “Is anything working?”

The better question is: “Is this working enough to become the company we are trying to build?”

Big promises raise the bar

Raising big early rounds at high valuations makes this trap worse.

A premium valuation can feel like validation. It tells the founder, the team, and the market that the company is special.

But premium valuations require premium results.

We learned a version of this at Moichor after our seed round closed.

At the time, I thought fundraising was about getting people to believe in the biggest version of the vision. Think big, sell the upside, show where the company could go if everything worked.

That part matters. Investors need to believe the upside is worth the risk.

But once the round closes, everyone starts watching the gap between what you said and what the company is actually doing.

If you raise on a huge promise, normal startup messiness starts to look like underperformance. A slower sales cycle. A delayed launch. A customer that needs more hand-holding. A product wedge that needs to shift. None of these are unusual at seed. But if the story was framed as breakout momentum, every lukewarm signal gets judged against that promise.

The better way is to present the business in two layers:

Base case: what you believe the company can realistically prove with the capital you are raising

Optimistic case: what could happen if the strongest signals compound

Then talk openly about the barriers to the base case. What has to go right? What could slow you down? What assumptions are still unproven?

That does not make the pitch weaker. It makes it more credible.

Because after the round, investors are not only watching whether you hit the goal. They are watching how you set the goal in the first place.

This matters a lot at pre-seed. If you raise at a $20M pre-seed, the next round is not judged like a normal pre-seed company. Investors are not just asking whether there is something interesting here. They are asking whether the company has grown into the price.

Investors almost always leave the door open. They will say they like the market, want to track progress, and would love to take another look when you raise the next round.

None of that is bad. It is often genuine.

But it is not conviction.

If you raised at a $20M pre-seed and you do not get to something like $1M ARR, or at least show a very clear path to that level of traction, your next round just became much harder. The investor who was “excited to stay close” may still like you. They may still think the team is strong. They may still believe the market is big.

But the question has changed.

It is no longer: “Could this become something?”

It becomes: “Why has this not broken out yet relative to the price?”

That pressure can make founders defend the original story right when they should be most open to changing it. The market may be saying, “There is something here, but not exactly this.” The valuation may be saying, “Prove the thing you already pitched.”

That tension is dangerous.

Force clarity earlier

The clearest way to separate promising from working is to ask whether learning is compounding.

Is each customer making the next customer easier? Not easy. Easier.

Are objections becoming more predictable? Is onboarding getting lighter? Is the product becoming easier to explain? Are customers pulling you toward the same use case? Is usage becoming less dependent on founder hand-holding?

These are signs that the company is learning its way into a repeatable motion.

The opposite is also revealing. If every customer requires a different explanation, a different product, a different onboarding flow, a different pricing structure, and a different definition of success, the company may still be searching.

That is okay. But founders need to be honest about the difference between search and scale.

Search is when you are still trying to understand the pattern.

Scale is when the pattern is clear enough to push harder.

A lot of startups get in trouble by scaling while they are still searching. They hire too early. They raise too much. They build too broadly. They turn every customer request into roadmap.

The move is not to become pessimistic. The move is to force clarity earlier.

Ask customers:

What would need to be true for this to become a yes?

Is this a top-three priority right now?

What happens if you do nothing?

Who owns the budget for this?

Would you pay for this today?

The answers may be uncomfortable, but they are useful.

If the customer has no budget, no urgency, no owner, and no consequence for doing nothing, that is not traction yet. It may be research. It may be a future customer. It may be a useful relationship. But it should not be treated like proof.

The same is true with investors. A thoughtful maybe is still a maybe. A long diligence process with no clear next step is still a maybe. A partner who “really likes what you are building” but will not commit is still a maybe.

A clean no is underrated because it gives the founder time back.

The job is to find out what is real

Every great company starts with weak signals: a few users, a weird customer, a small pilot, a product that barely works but solves one painful problem.

The best founders do not ignore those signals. They study them, but they also test them.

They ask whether interest is turning into urgency. Whether usage is turning into habit. Whether pilots are turning into expansion. Whether conversations are turning into decisions. Whether founder effort is turning into systems. Whether one customer is teaching them how to win the next ten.

That is the difference between promising and dangerous.

Promising is useful when it moves you closer to truth. Promising is dangerous when it becomes the reason you stop looking for one.

At pre-seed, we do not expect everything to be working. The company is still early, the product is still changing, and the market may still be forming.

But we do look for founders who can tell the difference between something that is getting closer to working and something that is simply getting better at consuming their time.

Because in the beginning, the job is not to look like you are making progress.

The job is to find out what is real.